Last week, Databricks raised a massive $10 billion Series J, during which they also disclosed some high level financials of their business. This, coupled with Snowflake being public, gives us the opportunity to compare the financials of these two, as I’m sure every growth fund that looked at the Databricks round did.

Overview and Key Metrics

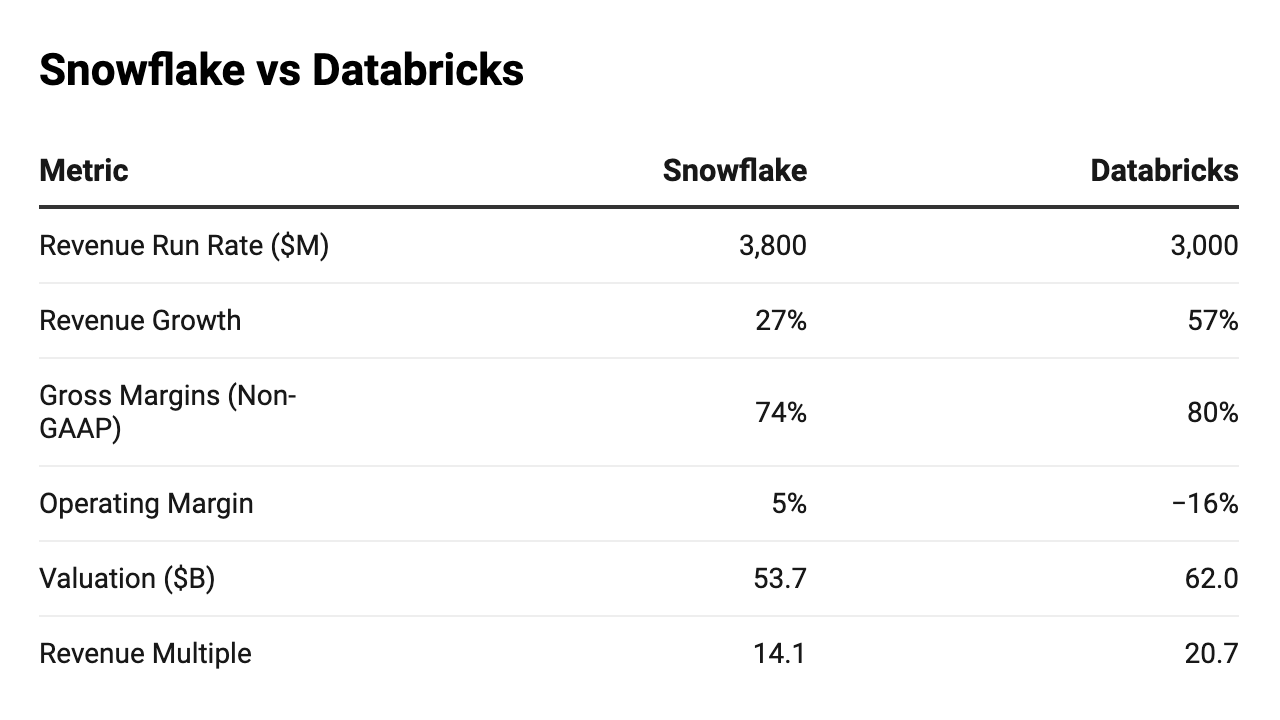

First, here’s just a quick overview of the key metrics between Snowflake and Databricks based on where they are expected to be at the end of their Q4 ‘24 (Jan 31 2025).

Snowflake is at a slightly larger revenue scale (26% higher revenue-runrate) and is more profitable, but Databricks is growing significantly faster and is more highly valued (albeit in the private markets compared to Snowflake being public).

Revenue and Growth

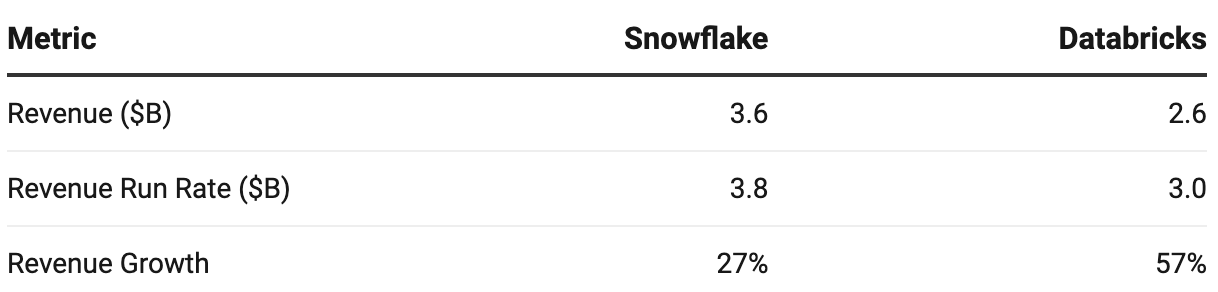

Let’s dig a bit deeper into revenue and growth first.

Snowflake and Databricks present contrasting growth stories:

- Snowflake: With $3.6 billion in revenue growing at 27%, Snowflake is scaling steadily while focusing on stability and profitability. The shift in emphasis over the past few years in the public markets to profitability over growth may have played a role in this.

- Databricks: At $2.6 billion in revenue and a 57% growth rate, Databricks continues to grow at a very impressive pace given its scale.

Depending on the durability of Databricks’ growth in particular, we could see them cross Snowflake in revenue sometime in Q1 of 2026, in the ~$4.5B range.

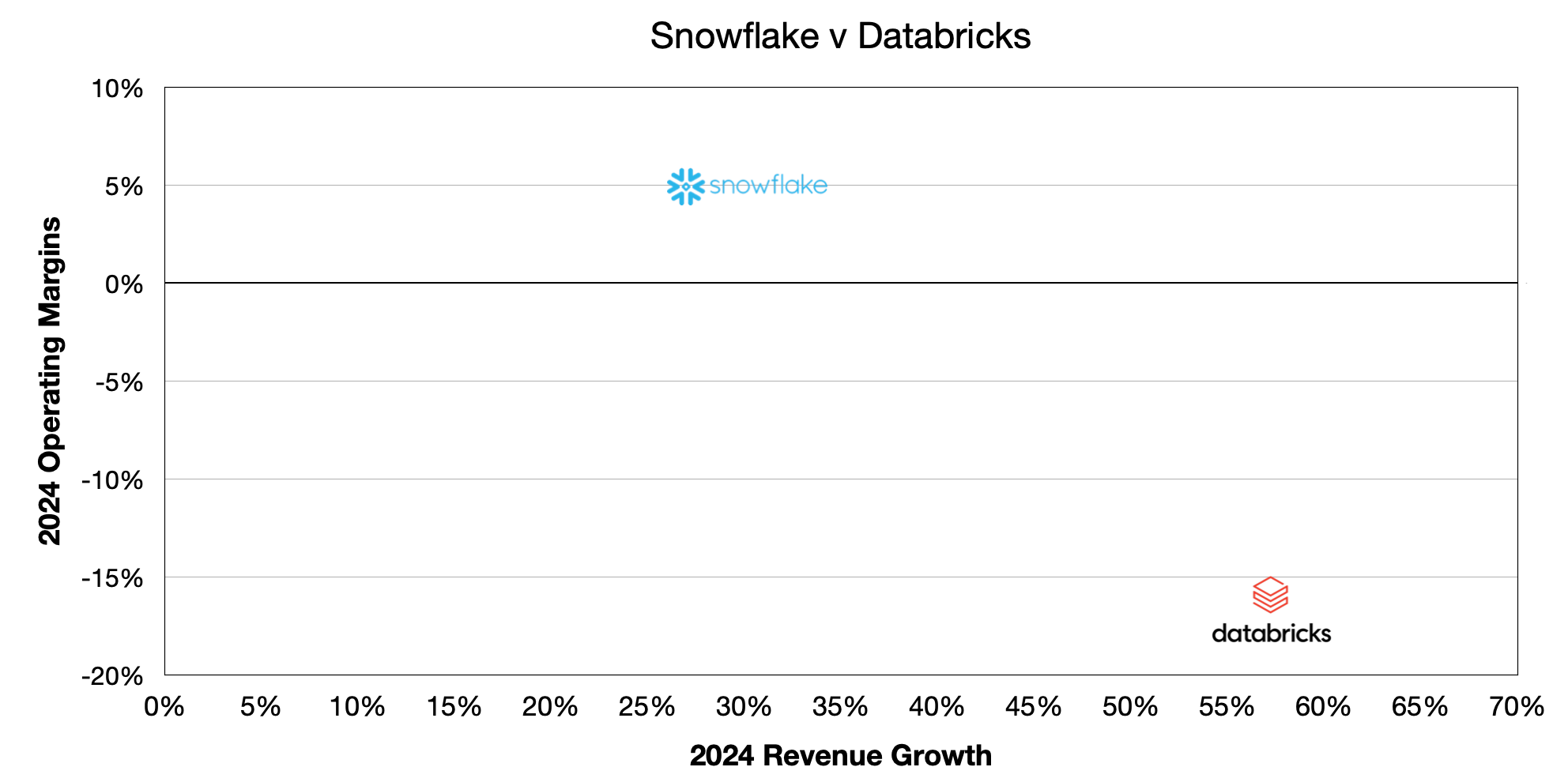

Profitability and Operational Efficiency

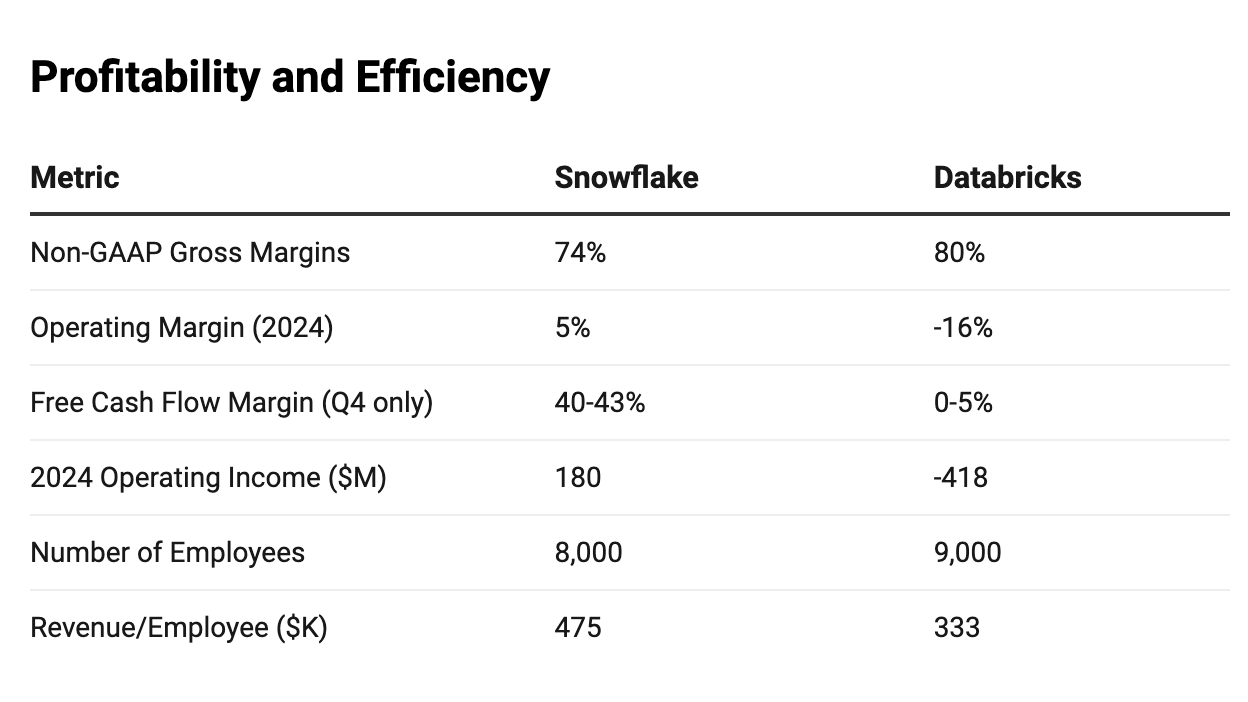

The table below compares their profitability and operational efficiency metrics.

Looking at the table above, we see the following:

- Snowflake: Snowflake is profitable on both an operating margin basis and is extremely free cash flow profitable (though the aggregate FCF margins across the year are closer to 20-25%) and are higher in Q4 due to timing of payments.

- Databricks: While Databricks notes higher non-GAAP gross margins (the caveat is that they may be calculated differently than Snowflake), it is still losing significant amounts of money, with operating losses expected ot be upwards of $400M in 2024. At the same time, they have made improvements on the margin front and they expect to be free cash flow profitable in Q4. While it’s unclear if it’s as seasonal as Snowflake, it is likely that databricks could be free cash flow profitable across 2025.

Overall, Snowflake is probably 20 percentage points or so ahead on the margin front to Databricks, and is operating at a slightly greater level of efficiency in terms of revenue/employee.

Valuation Metrics

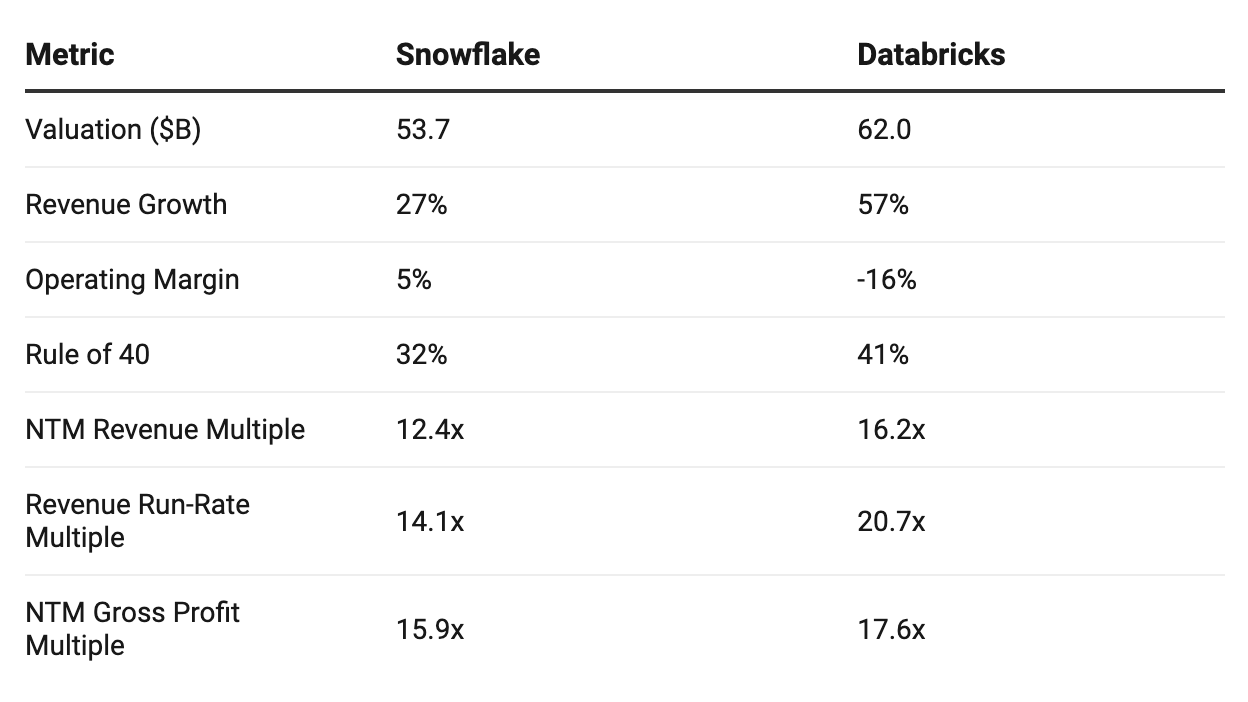

Both companies overall have quite favorable multiples compared to the rest of the software index, highlighting the quality of the two businesses.

Between the two, we see that Databricks currently is fetching a higher multiple with its much stronger revenue growth rate and better Rule of 401, in addition to what many investors believe is a better positioning for continued durable growth with the tailwinds in AI.

Snowflake is valued at 12.4x NTM revenue while Databricks is valued at a ~30% premium to that of 16.2x NTM revenue.

Closing Thoughts

To summarize on the financials, Snowflake today is at a $3.8 billion revenue run rate, 1.27x the revenue scale of Databricks at $3 billion run rate, but the latter is growing 57% compared to Snowflake’s 27%.

On profitability, Snowflake is about 20-25 percentage points more profitable than Databricks, although Databricks is also approaching free cash flow profitability as of this coming quarter.

In aggregate, Databricks has a higher Rule of 40 at 41% versus Snowflake’s 32%, and Databricks is valued 15% higher than Snowflake at $62 billion. On an NTM revenue multiple basis, Databricks is valued at a 30% premium to Snowflake, with a 16.2x multiple versus 12.4x for Snowflake.

Lastly, a few general observations between the two businesses that are worth highlighting:

- Public v Private: Databricks has been more aggressive these past few years, prioritizing investments in product development, sales expansion, and strategic acquisitions like MosaicML and Tabular. The much faster revenue growth supports this strategy and highlights the payoff from these focused efforts. How much of that is a function of them being private versus Snowflake being public? In the public markets, sentiment has shifted over time—initially prioritizing growth, then profitability, and more recently showing renewed interest in growth, particularly when coupled with an AI story. Snowflake has executed well in the context of a public company, growing reasonably while being profitable, while Databricks has leaned in more on growth, which has paid off for it.

- AI positioning: Databricks is certainly better positioned in the AI wave, given its original focus on ML workloads, unstructured data, and aggressive acquisitions of MosaicML and Tabular. These acquisitions have strengthened its capabilities in generative AI and machine learning, enabling it to offer more comprehensive solutions for unstructured data and advanced AI workloads. While Snowflake still has a reasonable multiple of ~12.4x NTM, a big part of both the faster growth for Databricks and the higher multiple comes from its stronger long-term positioning for continued growth in the AI era. While Snowflake has not been shy to invest either, with acquisition of Neeva and continued expansion of Snowpark capabilities, it will be interesting to see how they continue to move further beyond analytical workloads into AI workloads, particularly those based on unstructured data.

Note that I calculated Rule of 40 based on Operating Margin rather than FCF margin based on data availability, so in reality the two companies Rule of 40s likely look better, but this captures the relative difference.

To read more about my insights on Databricks, Snowflake, and all things business tech, check out my Substack.